If you’re considering the jump from W-2 employment to working as a 1099 CRNA, you’re not alone. The promise of more money, schedule flexibility, and personal freedom draws many CRNAs into independent contracting. But with that freedom comes responsibility. You’re no longer just showing up and getting paid. You’re running a business.

This guide answers the key questions every CRNA should ask before accepting a 1099 role. We’ll cover taxes, legal setup, retirement options, insurance needs, and how to avoid common mistakes. Whether you’re testing the waters or ready to go all in, this is your starting point.

Table of Contents

- W-2 vs 1099

- Understanding 1099 Taxes

- Do You Need a Business Entity

- Keeping Finances Separate

- Hire the Right CPA

- Retirement Strategies

- Insurance and PTO

- Legal and Contractual Risks

- Managing Income Variability

- Must-Have Backend Systems

- Protecting Yourself from Recruiters

- How to Transition to 1099

- Understanding Job Security

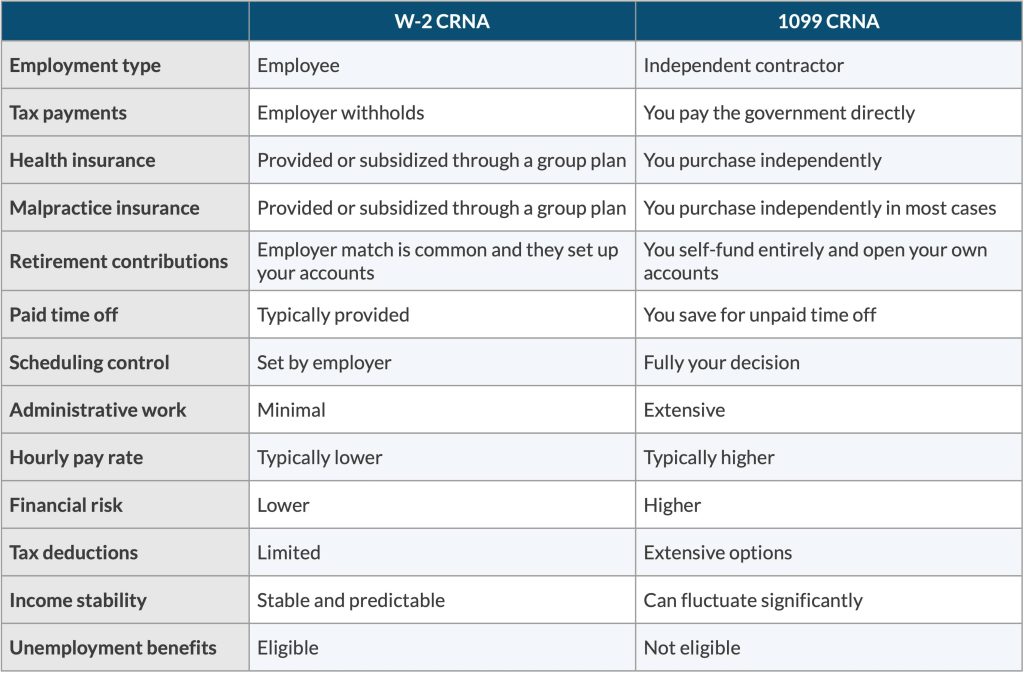

1. How is a 1099 CRNA Different from a Typical, W-2 Employee?

A W-2 CRNA is an employee. Taxes are withheld from your paycheck. Your employer may provide health insurance, malpractice coverage, a retirement match, and paid time off. You follow their schedule and face minimal administrative burden.

A 1099 CRNA is an independent contractor. You negotiate your pay, set your schedule, and manage everything behind the scenes—taxes, benefits, contracts, and compliance. You often earn more per hour, but you take on more risk and responsibility, not unlike self-employment situations.

2. Understanding Paying Taxes as a 1099 CRNA

When you go 1099, your tax responsibilities change significantly. Unlike W-2 employment, taxes are not withheld from your pay, so you’ll need to be aware and take proactive steps to comply with federal and state requirements.

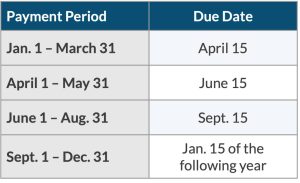

Estimated Quarterly Taxes

You must estimate and pay your federal and state taxes four times annually. The table below details when federal payments are due. State due dates don’t always align with the federal schedule.

Work with your CPA to calculate how much to pay each quarter based on your projected income. Many CRNAs set aside 25–35% of their income to cover taxes.

You can pay the IRS through the Electronic Federal Tax Payment System (EFTPS) or by mailing in Form 1040-ES. State estimated taxes are paid separately. Automating this process through your CPA or trusted tax software helps ensure accuracy and consistency.

Self-Employment Taxes

As a 1099 independent contractor, you’re considered self-employed. This means you’re on the hook for self-employment taxes, which are 15.3% of your net income. Net income equals income after deductions, highlighting the power of reducing taxable income through deductions (we’ll explore these in a later section). Here’s what’s included in self-employment taxes:

- 12.4% Social Security tax

- 2.9% Medicare tax

- 0.9% Medicare surtax for earnings above $200,000 (single) or $250,000 (married filing jointly).

You can deduct half of your self-employment tax when calculating your adjusted gross income (AGI), reducing your federal tax burden.

1099-NEC Forms

Instead of receiving a W-2 during tax season, each facility or anesthesia group paying you $600 or more annually will issue a separate 1099-NEC by January 31. Keep all these forms organized, and carefully track income throughout the year, verifying accuracy as you receive each form.

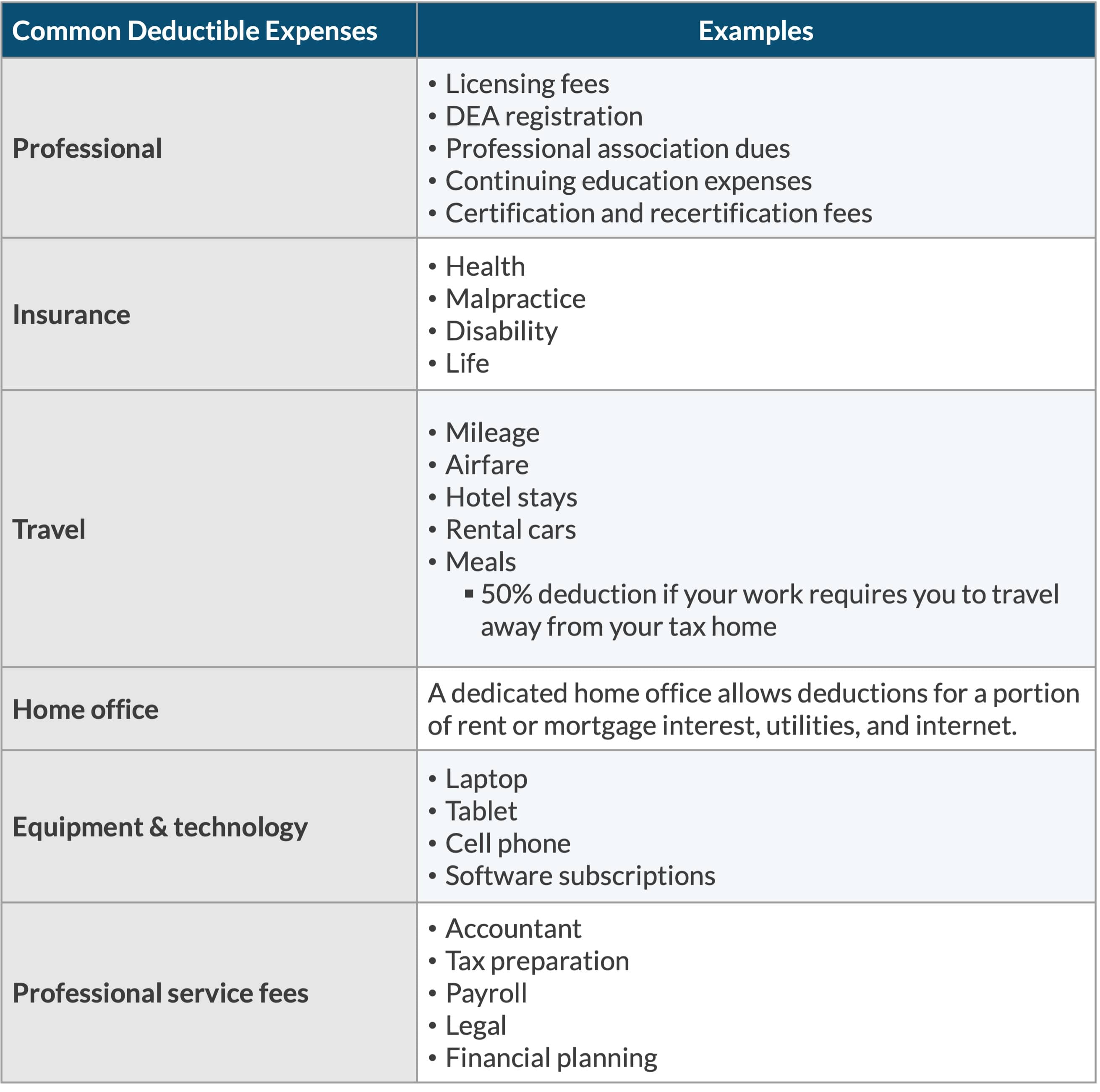

Tax Deductions

Business-related deductions are one of your most valuable financial advantages as a 1099 CRNA. Again, this article is for educational purposes only, and you should consult with your CPA to discuss your unique situation.

Also, here’s a common misunderstanding. Something is not necessarily tax-deductible just because your CPA says so. Although a CPA can provide valuable tax advice and guidance, it’s your responsibility to ensure that any deductions you claim are legitimate and supported by law and proper documentation. Tax attorneys can also provide expert guidance, but regardless of the guidance you receive, the IRS will have the final say in the event of an audit.

3. Do You Need a Business Entity?

Yes (in nearly all cases). Without one, you’re a sole proprietor, which means you and the business are considered one and the same. That means you won’t have liability protection, and your personal assets are at risk if someone sues your business.

Limited Liability Company (LLC)

An LLC offers liability protection and separates business from your personal finances. It also helps you establish a professional image with clients. In some states, a Professional Limited Liability Company (PLLC) may be a better option, so discuss this with your CPA. We’ll use LLC and PLLC interchangeably throughout this article.

S-Corp Election (LLC taxed as S-Corp)

Once your income reaches a certain threshold, electing S-Corp status may save you money on self-employment taxes by splitting your income into salary and distributions. This structure requires payroll processing and formal recordkeeping.

Here’s a list of other things you’ll need to keep your business legit:

1. Form the LLC Properly

- Choose an available business name

- Must be distinguishable and comply with your state’s LLC naming rules

- Check the USPTO to ensure the name does not have a federal trademark

- File Articles of Organization

- File with your Secretary of State

- Pay Filing Fee

- Varies by state (typically $50–500)

2. Get Identification and Records in Place

- Apply for a free EIN (Employer Identification Number)

- Create an operating agreement

- Not always required, but strongly recommended (especially with multiple members)

- Defines roles, ownership percentage, profit distribution, dispute resolution, and exit plans

3. Register for Any Required Local, State, or Federal Licenses

- Business licenses or permits

- May vary by state

- Professional licenses

4. Maintain Financial Separation

- Open a business bank account

- Never co-mingle personal and business funds

- Get a business credit card

- Builds credit and helps separate finances

- Set up accounting software or system

- For taxes, expenses, and income tracking

5. Other Considerations

- Register a registered agent

- Can be you, another person, or a company who accepts legal documents

- File foreign registrations

- If you do business in multiple states

- Insurance (research each to determine what’s best for you)

- Malpractice

- Professional liability

- Disability

- Life

- Workers’ comp

- Stay compliant over time (e.g., renewing your LLC, filing annual reports)

- Pay quarterly taxes

4. Keep Business and Personal Finances Separate

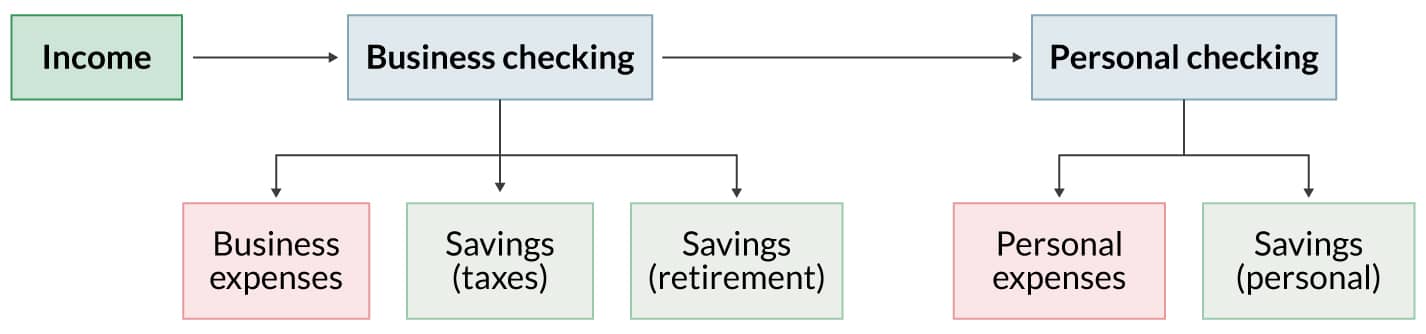

Separate your business and personal finances. All income, expenses, and tax payments should go through a dedicated business checking account. This keeps your records clean, simplifies tax filings, and makes navigating audits easier.

Business bank accounts also protect your legal structure. If you operate as an LLC or S-Corp and mix personal and business funds (often referred to as “co-mingling”), you risk “piercing the corporate veil.” This legal term means a court could disregard your business structure and hold you personally liable in a lawsuit against your business. The whole point of forming an entity is to protect your personal assets. Co-mingling funds breaks that barrier. Keep it clean.

Here’s an example of how to set up your accounts.

5. Hire the Right CPA Early

Once you decide to go 1099, you should form a relationship with a certified public accountant (CPA). This sets the foundation for your 1099 success by ensuring you’re making the right moves from the start.

The right CPA will:

- Help you choose the right business structure

- Calculate and schedule your quarterly tax payments

- Ensure compliance with state and federal tax laws

- Maximize deductions to reduce taxable income

- Set up and manage your retirement strategy

Choose someone with experience advising 1099 CRNAs or self-employed healthcare professionals. Some CPAs view their jobs as simply helping you file your taxes. The best ones help you with a comprehensive strategy to help you build wealth.

6. Retirement and Wealth-Building Strategies

As a 1099 CRNA, you have more retirement options and higher contribution limits than you did as a W-2 employee. These tools can help you reduce your tax burden while building long-term wealth. Depending on the vehicles you use, you could potentially save tens of thousands of dollars annually.

Solo 401(k): Allows contributions as both employee and employer, up to $69,000 annually (2024 limits). Contributions reduce taxable income.

Defined benefit plan: Acts like a personalized pension. Offers even larger contribution potential. Best suited for high earners. Requires actuarial support and a multi-year commitment. More expensive to administer but the tax savings are well worth it.

Backdoor Roth IRA: Allows high-income earners to access Roth IRA benefits. Coordinate carefully with your CPA to avoid triggering unexpected taxes.

Qualified business income (QBI) deduction: Allows eligible 1099 contractors to deduct up to 20% of their net business income. Only applies to certain types of income and phases out at higher income levels, so consult a tax professional to determine eligibility.

Health savings account (HSA): Triple tax benefit: 1) contributions are tax-deductible; 2) growth is tax-free; and 3) withdrawals are tax-free if used for qualified medical expenses. Paying for health expenses out of pocket (e.g., not dipping into your HSA) allows this money to compound over time.

S-Corp income splitting: If your LLC is taxed as an S-Corporation, you can split your income between a W-2 salary and owner distributions. You pay full payroll taxes on the salary portion, but distributions are not subject to self-employment tax. For example, if you earn $240,000, you might pay yourself a $130,000 salary and take the remaining $110,000 as a distribution, saving thousands in payroll taxes. This strategy can lead to significant tax savings, but you must pay yourself a “reasonable” salary. Your CPA will help determine an appropriate amount. Paying yourself too little to avoid taxes increases your risk of audit and back taxes.

These strategies can save you thousands of dollars in taxes each year and help you build lasting financial security. Work with a CPA or advisor who understands the unique needs of CRNAs to tailor the right approach for your business.

7. Insurance and Paid Time Off

You’re responsible for replacing all the benefits your employer previously provided. For an in-depth analysis of this topic, check out this article: Understanding CRNA Compensation and Benefits: It’s More Than Your Salary. At a high level, this includes:

Health insurance: Explore private plans, ACA marketplace options, or coverage through a spouse.

Malpractice insurance: Confirm policy type (occurrence or claims made), limits, and whether tail coverage is required.

Business liability insurance: Consider general or professional liability insurance to protect against non-clinical claims, especially if you operate as an LLC or S-Corp.

Disability and life insurance: Prioritize own-occupation disability coverage and term life insurance.

Paid time off: You won’t get paid when you’re not working, so budget for vacations, sick days, and unexpected downtime. It’s easy to discount the financial value of PTO (PTO value = Hourly rate × # hrs PTO). For instance, if your full-time W-2 salary is $225,000 and you get 8 weeks (320 hrs) of PTO, then the value of your PTO is ~ $35,000 ($110/hr × 320 PTO hrs). If you wanted 8 weeks off as a 1099, you’d need to factor this in to your billing rate (along with all of your other expenses).

The bottom line is that you need to build the cost of these benefits into your hourly rate and savings plan.

8. Legal and Contractual Risks

Before signing any 1099 agreement, carefully review the contract. Some CRNAs seek legal counsel, whereas others wing it. The recurring theme is that this decision comes down to your risk tolerance. Key areas to evaluate include the following:

- Cancellation clauses and termination notice

- Payment terms, including rate, frequency, and method

- Call and weekend expectations

- Whether malpractice insurance is provided or required

- Restrictive covenants such as non-compete clauses

- Indemnity clauses that shift legal responsibility for facility errors to you

- Non-solicitation clauses that may prevent you from working directly with a facility after a contract ends. Review carefully to avoid limiting future opportunities.

Some employers misclassify CRNAs as independent contractors (when they’re treated as W-2 employees) to save money on taxes and benefits. So, beware of long-term roles that function like W-2 jobs. The IRS is watching.

If the facility dictates your schedule, controls how you work, and restricts outside employment, the IRS may consider the role misclassified. If the IRS discovers misclassification, it can trigger audits, back taxes, and penalties for the employer (not you). But even if the employer is typically held liable, a misclassified CRNA may face loss of unemployment eligibility, difficulty collecting back pay, and potential tax confusion if reclassified retroactively.

9. Managing Income Variability

As a 1099 CRNA, you’ll experience income fluctuations. Build a buffer and plan ahead.

- Emergency fund: Save 3–6 months of essential expenses. Whether you’re the sole breadwinner or you have a partner with a stable income will influence your risk tolerance.

- Tax savings account: Transfer 25–35% of every payment to a separate account for taxes. Whatever is left over at the end of the tax year is yours to keep.

- Retirement contributions: Make automated, monthly contributions to stay consistent.

- Cash flow tracking: Use bookkeeping software or a spreadsheet to monitor income, expenses, and upcoming obligations.

Staying disciplined with money management protects your long-term stability.

10. Must-Have Backend Systems

You’ll need to run your business like a business. Set up these systems before you start:

- Separate business bank accounts: We discussed this earlier, but it bears repeating. Never mix business and personal funds! At a minimum, you should have business accounts for checking (for operational expenses) and savings for estimated taxes.

- Bookkeeping software: QuickBooks, Wave, Gusto, or a spreadsheet for tracking income and expenses. You can also use software to run payroll if you’re an S-Corp.

- Invoicing tools: Use professional templates or software to send timely invoices.

- Digital filing system: Organize contracts, licenses, receipts, and insurance documents for easy access and audit protection.

11. Protecting Yourself from Recruiters

Although many recruiters offer helpful opportunities, a few bad actors use tactics that hurt CRNAs and damage the reputation of the profession as a whole. Recruiters work for the agency, not for you. Protect your interests by being selective (research the CRNA forums online), asking tough questions, and getting everything in writing.

- Watch for rate suppression: Some recruiters deliberately offer below-market rates to keep more margin for themselves. Although they’re providing you a service (and deserve to get compensated), know your worth by benchmarking current regional pay.

- Avoid exclusivity clauses: Never sign contracts that restrict you from working with other agencies or facilities unless you’re compensated appropriately.

- Confirm malpractice coverage: If a recruiter claims to provide malpractice insurance, request the policy details in writing. Always verify limits (these vary among states), tail coverage, and whether the policy names you directly.

- Ask for full contract details upfront: Don’t accept vague job descriptions. Request a full contract before committing and read all terms, not just the pay rate. Some recruiters will request your resume before sharing job details. Be wary of this practice.

- Maintain your own network: Build direct relationships with facilities and trusted agencies. Relying on a single recruiter creates an unnecessary dependency.

- Protect your phone number: They’re going to text you, in some cases a lot! Only share your phone number after you’ve vetted the recruiter.

Stay in control of your professional identity. Keep a record of where your resume goes and who is representing you at each site.

- Watermark your resume: Add a discreet watermark with your name, contact info, and a statement like, “This resume is provided exclusively for consideration by [Facility Name]. Unauthorized distribution prohibited.” This discourages recruiters from shopping your resume without consent.

- Tailor your resume per submission: Create a separate PDF version for each opportunity with the facility’s name in the file name and body text. This clarifies that the document was submitted for a specific role and can help resolve disputes about who submitted your resume first.

- Control your resume: Never allow a recruiter to submit your resume to a facility without your explicit written permission. Some agencies will “claim” you at a facility by submitting your name without consent, which can block other recruiters (or even you) from applying directly.

- Use a disclosure policy: Ask to review and sign an agency’s disclosure agreement stating that they will not submit your information without prior approval. Keep written records of when and where your resume is submitted.

- Know the consequences of multiple submissions: If multiple agencies submit your resume to the same facility, some facilities will disqualify you from consideration entirely. Others may default to the first recruiter who presented you, which could lock you into a lower rate or less favorable terms.

12. How to Transition to 1099 Smoothly

You don’t need to go full-time 1099 overnight. Start small and scale as you become more confident that it’s the best path for you. Here are several things to consider:

- Accept PRN or short-term contracts first. If you moonlight, be sure you’re not violating your contract with your W-2 employer. Use your experiences to test your systems and gain experience.

- Work with your CPA to run tax projections and retirement planning before leaving your W-2 job.

- Ensure your state license, DEA registration, and credentialing files are current and complete before accepting your first 1099 contract. Some facilities require lengthy onboarding.

- Secure malpractice coverage before you work. Don’t wait until a contract is signed. Purchase your own malpractice policy early, especially if you’re working across multiple sites or states.

- Create a reusable file packet that includes your W-9, COI (certificate of insurance), CV, licenses, and other required documents. This streamlines your response to recruiters and facilities.

- Set a target hourly rate before negotiating. Know your breakeven rate, the amount you need to cover taxes, benefits, overhead, and personal financial goals. This helps you avoid undervaluing your services. On the flipside, understanding the economics of the local market will help you get a sense of your true value.

- When you’re offered a 1099 contract, you’ll often see two types of pay structures: hourly rate plus stipend to cover expenses (housing, travel, etc.) or all-inclusive rate. Work with your CPA to determine how each scenario impacts your tax liability and take-home pay. A seemingly higher all-inclusive rate may actually result in less after-tax income than a lower hourly rate paired with well-structured stipends. There’s no answer that’s always best, so evaluate each offer independently.

- Talk to other 1099 CRNAs. Ask about lessons learned, agencies they like, and red flags they’ve encountered.

Start with strategy, not urgency. The transition is smoother when it’s planned.

13. Understanding Job Security as a 1099 CRNA

One of the most overlooked tradeoffs of 1099 work is job security. When you’re a W-2 employee, you have more structural protection. Your schedule, income, and benefits are generally stable unless the facility goes through layoffs or restructuring. Even then, you may receive notice, severance, or be eligible for unemployment benefits.

By contrast, 1099 work is inherently less secure. As more CRNAs enter the 1099 market (supply side increases), there is greater competition that can drive down rates. Contracts can be canceled with little notice. Shifts may dry up. Facility needs can change overnight. CRNAs practicing during the economic recession of 2008 may recall that many 1099 positions disappeared virtually overnight in many parts of the country. Although no one can predict the future, history has a way of repeating itself.

Finally, since you’re not considered an employee, you have fewer legal protections and you’re generally not eligible for standard unemployment benefits. This doesn’t mean 1099 is too risky. It just means you need to execute a sound strategy.

Final Thoughts

Working as a 1099 CRNA can unlock more income, freedom, and long-term financial security, but only if you treat it like a business. With the right systems, support team, and mindset, you can take control of your career in a way most W-2 roles can’t support.

Start by investing in the right guidance, building your financial infrastructure, and planning your transition carefully. Your future self will thank you.

Check out the APEX Job Board when you look for your next W-2 or 1099 opportunity.

Related Articles